Understanding how to calculate monthly mortgage payment is essential for any homeowner or prospective buyer. Your monthly payment determines affordability, long-term planning, and your overall financial strategy. Whether you’re buying your first home, refinancing, or planning your budget, knowing exactly how to calculate your mortgage payment can save you stress and money.

In this detailed guide, we’ll explore the formulas, break down the components of your mortgage, provide practical examples, and answer frequently asked questions about how to calculate monthly mortgage payment.

What Is a Monthly Mortgage Payment?

A monthly mortgage payment is the amount you pay every month toward your home loan. It typically includes:

- Principal: The portion of your payment that reduces your loan balance.

- Interest: The cost of borrowing from the lender.

- Taxes: Property taxes assessed by your local government.

- Insurance: Homeowners insurance to protect your property.

This is often summarized as PITI (Principal, Interest, Taxes, Insurance). When calculating monthly mortgage payments, most people start with principal and interest, then add taxes and insurance later for the total cost.

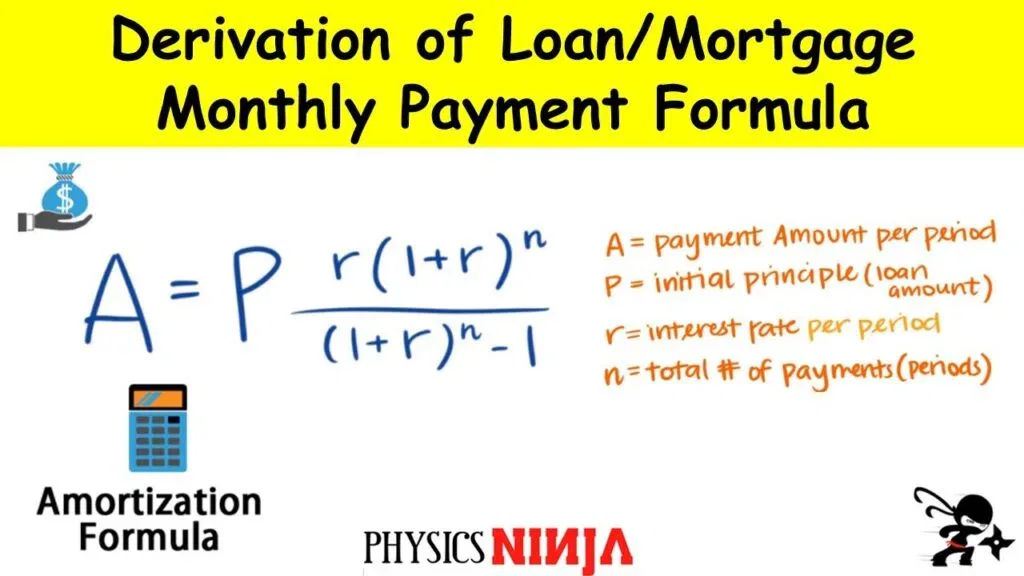

Step 1: Understanding the Mortgage Formula

The standard formula for calculating a fixed-rate mortgage payment is:M=P(1+r)n−1r(1+r)n

Where:

- M = Monthly mortgage payment (principal + interest)

- P = Principal loan amount

- r = Monthly interest rate (annual rate ÷ 12)

- n = Total number of payments (loan term in months)

This formula calculates the payment needed to fully pay off the loan by the end of the term, accounting for interest.

Step 2: Determine Your Loan Details

Before calculating your payment, gather the following information:

| Component | Description |

|---|---|

| Loan Amount | Total mortgage principal you are borrowing |

| Annual Interest Rate | Lender’s interest rate for the mortgage |

| Loan Term | Length of your mortgage in years (commonly 15 or 30) |

For example, a $300,000 loan at a 6% annual interest rate for 30 years would use:

- P = 300,000

- r = 0.06 ÷ 12 = 0.005

- n = 30 × 12 = 360 months

Step 3: Apply the Formula

Using the formula:M=300,000(1+0.005)360−10.005(1+0.005)360

Step-by-step calculation:

- 1+r=1+0.005=1.005

- (1+r)n=1.005360≈6.022575

- r(1+r)n=0.005×6.022575≈0.0301128

- (1+r)n−1=6.022575−1=5.022575

- Divide numerator by denominator: 0.0301128 ÷ 5.022575 ≈ 0.005995

- Multiply by principal: 0.005995 × 300,000 ≈ $1,798.50

So, the monthly payment for principal and interest is approximately $1,798.50.

Step 4: Add Taxes and Insurance

Property taxes and homeowners insurance vary by location:

| Component | Monthly Amount |

|---|---|

| Property Taxes | $250 |

| Homeowners Insurance | $100 |

| Total PITI | $1,798.50 + $350 = $2,148.50 |

The total monthly mortgage payment, including principal, interest, taxes, and insurance, would be $2,148.50.

Step 5: Consider Additional Costs

Other costs can influence monthly payments:

- Mortgage Insurance (PMI): Required for down payments less than 20%.

- HOA Fees: Monthly fees for community associations.

- Escrow Adjustments: Some lenders adjust payments for property tax changes.

Adding these can increase the total monthly payment.

Step 6: Use an Online Mortgage Calculator

If manual calculations seem complex, online mortgage calculators are convenient tools. They allow you to:

- Enter loan amount, interest rate, and term.

- Include taxes, insurance, PMI, and HOA fees.

- Instantly see monthly payments and amortization schedules.

Even though calculators simplify the process, understanding the formula ensures you know what factors drive your payment.

Step 7: Amortization Schedule

An amortization schedule shows how each payment reduces principal and pays interest over time. For example:

| Month | Payment | Principal | Interest | Balance |

|---|---|---|---|---|

| 1 | $1,798.50 | $298.50 | $1,500.00 | $299,701.50 |

| 12 | $1,798.50 | $315.00 | $1,483.50 | $295,800.00 |

| 360 | $1,798.50 | $1,789.00 | $9.50 | $0 |

Early payments mostly cover interest, while later payments reduce the principal. Understanding this helps you plan refinancing or extra payments.

Step 8: Strategies to Reduce Monthly Payments

- Increase Down Payment: Reduces principal, lowering the monthly payment.

- Shorten Loan Term: 15-year loans reduce interest but increase monthly payments.

- Refinance at Lower Rates: If rates drop, refinancing can lower payments.

- Shop Lenders: Different lenders may offer slightly different rates.

- Make Extra Principal Payments: Reduces total interest and shortens loan term.

FAQs on How to Calculate Monthly Mortgage Payment

Q1: Can I calculate my mortgage payment without a calculator?

A1: Yes, using the formula provided, though it involves exponential calculations. Online calculators simplify the process.

Q2: Does this calculation include taxes and insurance?

A2: The formula calculates principal and interest only. Add taxes, insurance, and other costs for the full monthly payment.

Q3: How does loan term affect the payment?

A3: Longer terms (30 years) reduce monthly payments but increase total interest. Shorter terms (15 years) increase monthly payments but reduce interest.

Q4: What is amortization?

A4: Amortization is the process of spreading out your loan payments over time, showing how much goes to principal versus interest.

Q5: How does my credit score impact payments?

A5: A higher credit score typically secures a lower interest rate, which reduces the monthly payment.

Q6: Are adjustable-rate mortgages harder to calculate?

A6: Yes, because rates change periodically. You can calculate initial payments, but future payments may vary.

Q7: Can I include HOA fees in this calculation?

A7: Yes, add monthly HOA fees to the PITI total for a complete monthly cost.

Conclusion

Knowing how to calculate monthly mortgage payment empowers you to plan effectively, compare lenders, and make informed financial decisions. By understanding the formula, accounting for taxes and insurance, considering loan terms, and exploring refinancing opportunities, you can optimize your home financing strategy.

Whether you do it manually or use a calculator, having a clear grasp of your monthly mortgage payment ensures confidence when buying a home or managing your existing mortgage.